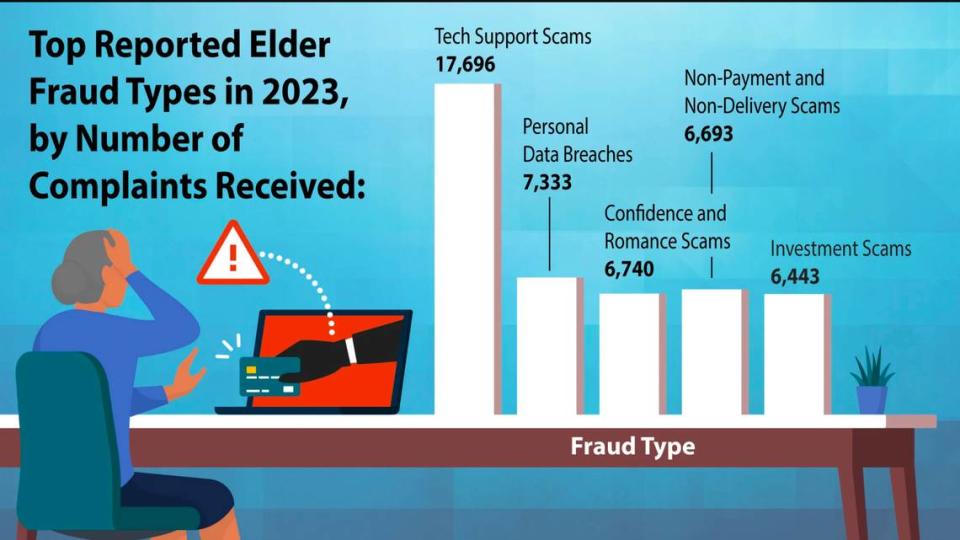

Raleigh police have seized hundreds of thousands of dollars in cash from cryptocurrency ATMs after successful scams using the sites. But the problem is much larger than one North Carolina city.

Between 2022 and 2023, the number of crypto-crime victims reported to law enforcement grew from nearly 1,000 to almost 1,500 in North Carolina, according to the FBI’s Internet Crimes reports.

Given the rising threat, here’s what you need to know about ATMs, cryptocurrency and keeping your money safe.

Lots of crypto ATMs

Like any other ATM, crypto ATMs are physical kiosks where people can make financial transactions. But with these, people can use U.S. currency to purchase bitcoin and other digital assets.

They usually accept cash and credit cards and can offer a number of cryptocurrency types for purchase, including bitcoin, ethereum, litecoin and more. At some kiosks, a user can only buy cryptocurrency. At others, they can buy and sell.

Users generally need to log into an account, select the type and amount of crypto they want to purchase or sell and provide identification. That identification can include inputting a code sent to a mobile device or letting the kiosk take a picture of the user with their driver’s license.

Many kiosks also employ “scam checks” during the transaction, flashing warnings on their screens about the risks of getting scammed.

Springing up around the U.S. over the last decade, cryptocurrency ATMs are found at convenience stores and gas stations. There are more than 1,000 of them in North Carolina, according to Coinatmradar, which the Government Accountability Office cited in a 2022 report.

There are at least 360 such kiosks in Raleigh, according to the website.

No current count is exact. The Financial Crime Enforcement Network, a branch of the U.S. Treasury Department that regulates the ATMs, doesn’t require cryptocurrency ATM operators to report the location of every machine they run.

Why scam with cryptocurrency?

Unlike dollar bills or personal checks, cryptocurrency is virtual cash not backed by any central organization, like a government or a bank. Users hold cryptocurrency in “wallets,” which are tied to ID codes that often reveal nothing about their owners.

Cryptocurrency promises “cross-border value transfer at the speed of the internet,” said Ari Redbord, global head of policy at TRM Labs, a blockchain intelligence company.

That’s something scammers use to their advantage, he said.

“Bad actors can receive crypto in faster and larger amounts, which sort of has blown up the scale of the problem,” Redbord said.

Cryptocurrency transactions are also difficult to reverse, Georgia Tech Professor Brendan Saltaformaggio said.

“There’s no one who’s centrally in charge or responsible for that transaction itself,” he said. “So there’s no one to go to and say, ‘Hey that transaction was fraudulent — you need to reverse that.”

There are one-off examples of cryptocurrency users collectively deciding to revert entire ledgers, said Kim Grauer, head of research at Chainalysis, another blockchain research firm. It happened to bitcoin in 2010 and ethereum in 2016. Cryptocurrency exchanges can sometimes freeze assets as well, Grauer added.

But those transaction reversals are few and far between, Saltaformaggio said. Scammers can use international cryptocurrency exchanges that don’t cooperate with U.S. law enforcement or host their cryptocurrency wallets individually.

“In those cases, there is no one who can be compelled to send that money back,” Saltaformaggio said.

Tough to catch scammers

When cryptocurrency changes hands, those transactions are recorded on a decentralized ledger called the blockchain. Because of how they’re programmed, ledgers are public and unchangeable.

Those public ledgers can ease parts of fraud investigations, Grauer and Redbord said.

“All of the transaction evidence is available in one place,” Grauer said.

Companies like TRM can comb through those transaction lists, flagging wallet IDs that are known to be tied to scammers, criminals and terrorists. Researchers like Saltaformaggio also use machine learning to tie wallet IDs to their owners.

With that information, law enforcement can try to catch the scammers or recover the defrauded money. In practice, recovery is the more feasible goal, Redbord said.

Generally, scammers try to off-ramp cryptocurrency quickly into traditional currency, Redbord said. Law enforcement races against the clock to stop the fraudsters when they process stolen cryptocurrency at an exchange.

Still, scammers can avoid authorities by jumping into multiple cryptocurrency wallets, some of which are not traceable on the internet, said James Kaylor, said FBI Special Agent James Kaylor, who supervises white collar crimes investigations in the Raleigh area.

Cooperation from foreign governments or companies also isn’t guaranteed, Saltaformaggio said.

“It’s not hopeless,” he said. “But it’s very difficult.”

Prevention is the best protection

Scam prevention is key, Redbord said. Here are strategies to keep yourself safe:

-

Don’t send cryptocurrency to someone you don’t know.

-

Report suspicious solicitations and threats. Remember: governments and businesses won’t pressure you to send cryptocurrency.

-

Inform law enforcement if you believe you have been scammed.

-

Don’t put any more money into cryptocurrency than you are willing to lose.

-

If you buy cryptocurrency, use exchanges with strong account owner identification and money laundering prevention. Check for software that labels and blocks suspicious cryptocurrency wallet IDs.

Ultimately, cryptocurrency ATM scams are an old trick with new technology (think Nigerian Prince).

“The same red-flag indicators of a scam that you will learn about in the financial world apply to cryptocurrency,” Grauer said.

Credit: Source link