Blockchain Lawyer Irina Heaver recently tweeted that the Central Bank of UAE has banned crypto payments in the country. Although there os no clear regulation for payments for goods and services in cryptocurrencies in the UAE, dollar-pegged stablecoins are actively used there. In this article, I’ve tried to discover the present and future of stablecoin regulation in the UAE and worldwide.

What happened in the UAE?

On the 3rd of June, the Central Bank of UAE held a meeting where they discussed, among other things, a new rulebook dedicated to stablecoins. The meeting agenda was dedicated to UAE’s Financial Infrastructure Transformation (FIT) program, including the future issuance of CBDCs and the development of the Emirates’ digital economy. A short overview of the meeting was published here.

In the beginning crypto community took this event quite positively—like the UAE will officially allow crypto payments in local stablecoins backed by AED. However, it looks like the situation is different and payments in other stablecoin (like USDT, USDC) for goods and services will be banned. In the published Rulebook on “Payment Token Services Regulation”by UAE’s CB is stated that “No Merchant or other Person in the UAE selling goods or services… may accept a Virtual Asset towards payment for that sale unless that Virtual Asset is a Dirham Payment Token issued by a Licensed Payment Token Issuer being used as a Means of Payment”.

At the same time, the Central Bank’s ruling should be perceived in the context of the UAE’s already existing legislation. Another local crypto regulator in UAE – VARA, has published a rulebook dedicated to virtual assets issuance in October 2023. In the document VARA has presented a new legal concept of “Fiat-Referenced Virtual Assets (“FRVAs”). Based on the rulebook VARA (and not CB UAE) is the regulator for all FRVAs except stablecoins backed by AED.

What does this mean for Crypto in the UAE?

By the way, these two facts only mean that there is a legal gap between the positions of the two UAE regulators in the field of crypto payments. Indeed, the Central Bank of UAE is supposed to be the country’s supreme regulator of payments. However, as long as the regulators do not clarify, we should not panic.

\Last but not least, the Central Bank doesn’t regulate settlements inside the Dubai International Financial Center (DIFC). However, the free zones have a significant impact on international trade and settlements between legal entities in Dubai. Based on this, there is a fairly high probability that at least for free zones there will be an option to carry provide payments in stablecoins pegged to foreign currencies.

Great Numbers Need compliance: a short overview of stablecoin regulations.

I already had provided an overview of global stablecoin regulation updates and it was published on Hackernoon. In short, more strict regulations on stablecoins are becoming an international standard. FATF, Financial Stability Board, IMF, and other organizations

repeat this over and over again in their documents. Naturally, large jurisdictions like Dubai need to match this.

The licensing framework for stablecoin issuers already exists in Japan, Singapore, the EU, and two popular offshores – Bermuda and the Bahamas. The United Kingdom and Hong Kong are planning to adopt the same rules. Draft legislation in the form of the

In general, the regulatory approach in most jurisdictions is similar – it establishes rules for stablecoins’ payments in terms of AML and compliance. In particular, stablecoin issuers must be licensed and provide complete information about their operations. Requirements for reserves are also specified.

There is also a trend to limit payments in foreign stablecoins. At least European exchanges have already announced restrictions on settlements in USDT since Tether has no plans to obtain a license in the EU. However, the USDC issuer Circle still remains available for European customers, and it plans to continue its activities in the eurozone under MICA.

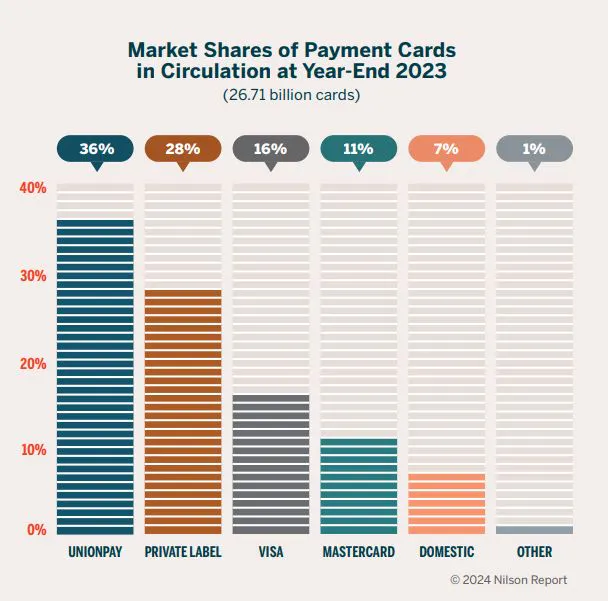

The volume of crypto payments in the world is growing at a rapid pace. Already, in 2022, annual settlements in USDT exceeded $18.2 trillion, while VISA had $7.7 trillion, and Mastercard had $14.1 trillion. Based on the image below, Visa and Mastercard account for 26% of the world’s card payments market together. In addition, data shows that the volume of SWIFT transactions for 2022 amounted to much more—$150 trillion.

In general, we can give a rough estimate – that Tether (the largest stablecoin) has become one of the important and large international payment systems. That’s why regulators’ attention, from the AML point of view, is growing toward stablecoins. In addition, central banks are worried that dollar-denominated stablecoins may displace local currencies.

Conclusion

By the way, more and more countries are formally banning crypto payments – for example, according to my information, they are banned in Georgia and Thailand. So far, too little time has passed since the publication of CB UAE’s rulebook. And it is not very clear how it will be implemented in practice.

In addition, CB UAE allows the purchase of virtual assets using foreign stablecoins. So, even if crypto payments are formally banned in Dubai, merchants can provide settlements through brokers and exchanges licensed in the country.

However, it’s possible for payment providers to provide auto-convert functionality for foreign stablecoins. This may include the ability to pay using a crypto balance or top up a crypto card with a dollar-pegged stablecoin and then pay with this balance for goods and services.

If you are interested in getting more crypto regulation insights, you can watch the global crypto regulation rating here and get updates on my Telegram channel.

Credit: Source link